- A focus on Africa

- Islamic finance

- A new world for the insurance industry

- SMP opportunities in Africa require local expertise

Business in Africa

In the past ten years, African countries have experienced unprecedented growth rates, with seven of the top ten fastest-growing economies in the world being those of key African countries

Africa is a continent of with a wealth of opportunities and potential, but along with the optimism and excitement are many inadequacies and challenges that still need to be addressed.

A focus on Africa

The investor spotlight shines brightly on Africa with its abundance of natural resources and recent mineral, oil and gas discoveries, demographic and political shifts and a more investor-friendly environment. Lynn Grala reports

Although the African continent faced many challenges in 2014 – such as the kidnapping of 276 schoolgirls in Nigeria, the Ebola outbreak in West Africa, and conflicts in various other countries – the continent continued to make economic headway with several African countries seeing growth and significant economic transformation, particularly Mozambique, Rwanda and Ethiopia.

The perception of Africa’s attractiveness as an investment destination is changing. Among Forbes survey results, from ranking eighth out of ten regions in their first survey to fifth in each of the next two surveys, Africa ranked second overall in 2014, after Nigeria. The Deloitte 2014 CFO survey also revealed that 80% of South African respondents said their company intended to expand into the rest of the continent in 2015 – a substantial increase from the 55% in 2013. This remarkable progress in a short space of time shows how the image of Africa has begun to change.

GROWTH IN AFRICA

Owing to protracted strikes, low business confidence, and a depreciating rand, growth slowed notably in South Africa. A slight recovery is expected this year through improving labour relations and gradually stronger exports. Although South Africa is now the continent’s second largest economy, it remains its most advanced economy.

By contrast, economic activity strengthened in Nigeria, the continent’s top oil producer and largest economy. It may experience one of the most accelerated growths, forecast at 7,3% in 2015.

Interesting to note is that Nigeria currently has the most newly registered companies in Africa yearly, with 70 000. South Africa is second with 30 000 a year and Kenya third with 22 000.

Growth remained robust in many of the continent’s low-income countries, notably Côte d’Ivoire, Ethiopia, Mozambique, and Tanzania. In Côte d’Ivoire, for example, a strong increase in cocoa production and rice output boosted agriculture growth and helped to sustain the country’s high growth. Ethiopia’s robust growth continued to be supported by agriculture, as well as by public investment, particularly in infrastructure.

This year it is forecast again to be a high performer with real GDP growth expected to remain around 7%, owing largely to the strong performance of the agricultural sector.

A wide range of African countries have now experienced consistent and robust growth for over a decade. Since 2002, the size of the overall African economy has more than trebled. What makes this economic performance all the more remarkable is that more than half of the decade has been marked by a deeply troubled global economy.

In the past ten years, African countries have experienced unprecedented growth rates, with seven of the top ten fastest-growing economies in the world being those of key African countries this year.

EASE OF CONDUCTING BUSINESS

The World Bank and IFC’s Doing Business 2012 listed the following African countries, in ranking order, by how easy it was to conduct business within their borders:

1 Mauritius

2 South Africa

3 Rwanda

4 Botswana

5 Ghana

6 The Seychelles

7 Namibia

8 Zambia

9 Uganda

10 Kenya

The Word Bank compiled this list on the basis of the following criteria: availability of electricity; how easy it is to register property; what kind of investor protection is available; what taxes are involved; how effectively contracts are enforced; how insolvency is resolved; whether construction permits are difficult to obtain; as well as the other intricacies involved in starting a business and employing workers.

The World Bank’s latest African Pulse, the organisation’s bi-yearly analysis of Africa’s economic status and subsequent prospects, has attributed this growth rate to the increasing investment in natural resources and infrastructure, as well as strong household spending in recent years. Not only have the more obvious resource-rich countries such as Sierra Leone and the Democratic Republic of Congo experienced high levels of growth, but also countries that are improving their political stability (like Mali), as well as those not rich in resources, namely Ethiopia and Rwanda.

Ease of doing business is not everything though, and this is reflected in the list of the top ten African countries in which foreigners should invest:

1 South Africa

2 Nigeria

3 Angola

4 Mozambique

5 Ethiopia

6 Tanzania

7 Ghana

8 Botswana

9 Mauritius

10 Kenya

Factors that make these countries attractive to investors are that they have established functioning free markets, offer large potential markets owing to their large populations, and boast huge raw material bases, as well as abundant and inexpensive labour forces.

KEY PRINCIPLES FOR DOING BUSINESS

Greg Davis, CFO Africa at the Standard Bank Group, recently shared some key principles for doing business in Africa. He says that doing banking and finance in Africa is not a big shift from doing it in the rest of the world, especially with the significant foreign direct investment being channelled into the continent lately, including investment from all the globally recognised accountancy bodies and professional services firms.

As a team, the Standard Bank Group cover 19 countries with finance staff situated in all of them and follow their 4i principles to ensure they are:

• In control

• Interacting

• Influencing, and

• Getting the most out of their infrastructure

Davis believes it’s important that you take opportunities and manage risk driving top and bottom line growth, which is done by focusing on the 4i principles. Focusing on the first i, being in control, he says it’s easy to lose control in Africa, so he likes to break this down in manageable chunks:

- On the ground accountability and control: Having the right people in the right place is the most important part of being in control. This means having fully empowered chief financial officers in every legal entity with full accountability for the controls in that legal entity

- Reconciliations: Ensuring all reconciliations are undertaken and reported. This is important in an environment with millions of transactions a month and multiple product systems

- Substantiation: Ensuring all balances are fully substantiated goes further than reconciling

- Self-assurance: Ensuring you have the right control framework and the right controls in place means reviewing them regularly and evidencing such. Doing this is often a way of standing back and realising you can improve your processes for controls or efficiencies

- Internal audit: Using internal audit as a truly value adding function that supports an effective control framework is important. You need to place reliance on your self-assurance and use internal audit to drive improvements rather than flying blind until Internal Audit undertakes audits. It is your control environment and not Internal Audit’s

- External audit: The quality of external audit firms is strong and the investment in people can be seen across the continent. Building good relationships with these firms in the country and globally is important not just for annual audits but process improvements and standardisation to the organisation

- Customer experience: All of this focus on controls and being in control ultimately improves the customer experience and safeguards their important assets. The closer finance is to the ultimate customer the better they can support the organisation

NEXT TEN BIGGEST CITIES

PwC economists believe the “Next 10” biggest cities in sub-Saharan Africa should be exciting investors too. It is predicted that by 2040, Africa is expected to have the biggest labour force in the world and experiencing faster economic growth than any other region. The population of these cities is projected to almost double by 2030, growing by around 32 million people. In fact, latest UN predictions show that by 2030 two of the Next 10 could have bigger populations than London has now.

INFRASTRUCTURE NEEDS

These strong levels of economic growth have led to an expansion of industry, commerce and per capita income which in turn has fuelled demand for infrastructure services including energy, transportation, ICT, water supply, and growing agriculture and urban infrastructure.

Infrastructure plays a key role in economic growth and reducing poverty having a 5–25% per annum return on investment as an economic multiplier, therefore the need to improve infrastructure and drive economic development is undisputed. Africa has an infrastructure gap of about US$35 billion a year.

PwC’s Capital projects and infrastructure in East Africa, Southern Africa and West Africa features interviews with 95 key players in the infrastructure sector, including development finance institutions, private financiers, government organisations and private construction and operations companies across East, West and Southern Africa. The sectors surveyed included water, transport and logistics, energy, mining, telecoms, and real estate, with the main focus being on economic infrastructure.

Respondents were optimistic about the continent’s infrastructure development, but a number of obstacles that must be dealt with. Resolving these quickly will not only positively affect their current projects, but more importantly, will attract other project developers, owners and investors to enter the African market.

Many projects across sub-Saharan Africa have also been affected by the lack of funding or insufficient funding. Funding from sources such as sovereign wealth funds, bonds and pensions funds is becoming increasingly important, but these types of investors are typically more interested in projects that are fully operational and tend to shy away from greenfield projects and their construction risks. China has made numerous investments across sub-Saharan Africa to support its need for resources. Japan, India and other Asian countries are also investing in infrastructure often linked to resources on the continent. Funding from local players is also increasing significantly.

PROMOTING REGIONAL INTEGRATION

Regional integration is another key to Africa’s prosperity. World leaders met recently in Geneva at the World Investment Forum, which was hosted by the UN Conference on Trade and Development to share policies and strategies for boosting investment and infrastructure to support sustainable development across the world.

Africa’s leaders need to leverage such comparative economic advantages by promoting region-building and regional integration, which are essential to sustainable development. Most African economies remain weak and historical divisions have worked against effective regional integration while institutional capacity has been lacking for national, subregional, and continental bodies promoting regionalism.

In pursuit of greater integration, African policy-makers need to advance their efforts to promote peace, security, and socioeconomic development. They also need to strengthen the capacities of institutional frameworks for intra-African trade, including through improved coordination between the AU and subregional bodies. The preoccupation of individual African governments with national problems has further slowed the progress of regional integration. Some governments have also failed to put in place efficient and effective domestic mechanisms for monitoring the consistency of national policies with regional frameworks.

YOUTH UNEMPLOYMENT AND TRAINING

Another problem is inadequate “soft” infrastructure like schools and universities, as well as youth unemployment. Though data unavailability and informal economic activity make estimates difficult, youth unemployment rates in sub-Saharan Africa are believed to hover around 30–50%, and even higher in parts of North Africa. The World Bank puts the figure at 38% in Nigeria, while the Economist projects 55% for young black South Africans. This is set against the backdrop of a fast-growing youth population, which is expected to double from a base of 200 million by 2045.

Companies and entrepreneurs can bring a sustainable solution while unlocking massive economic opportunity, but a change is required from today’s status quo. In June 2013, Harvard Business School launched a social enterprise, West Africa Vocational Education (WAVE), which targeted the youth unemployment issue. They identified two issues: the jobs gap and the skills gap. African companies need to take training more seriously; they need to step back and re-think their training strategies as a good training strategy is directly linked to reducing the unemployment problem.

In summary, Africa is a great source of growth opportunities for investors and although there are still major hurdles that need to be overcome, the good news is that perceptions about the continent that have often remained stuck in the past indeed appear to be changing.

Sources

Bryan Mezue, Africa’s companies need to become more like training schools, Harvard Business Review, 3 January 2014, https://hbr.org/2014/01/africas-companies-need-to-become-more-like-training-schools.

Dawn Nagar and Rosaline Daniel, Regional integration is the key to Africa’s prosperity, Business Day Live, 15 December 2014, http://www.bdlive.co.za/opinion/2014/12/15/regional-integration-is-the-key-to-africas-prosperity/.

Deloitte, CFO 2014 Report, http://www2.deloitte.com/content/dam/Deloitte/za/Documents/finance/ZA_CFO_Southern_Africa_15102014.pdf.

Greg Davis, Standard Bank: Four principles for doing business in Africa, CEO South Africa, http://cfo.co.za/profiles/blogs/greg-davis-standard-bank-4-principles.

KPMG, Africa’s Top 10 fastest growing economies, http://www.blog.kpmgafrica.com/africas-top-10-fastest-growing-economies/.

Yogesh Gokool, Africa’s economic outlook for 2015: how we made it in Africa, http://www.howwemadeitinafrica.com/africas-economic-outlook-for-2015/45777/.

Author : Lynn Grala is the Editorial Administrator of Accountancy SA

Islamic finance

A decisive opportunity for the African continent is on offer. Conventional finance mechanisms have demonstrated inadequacies and challenges in responding to the full realisation of the African opportunity. By Zuhdi Abrahams

Amid the economic volatility that has characterised market sentiment and influenced public policy around the globe over the past few years, one constant has been that the balance of economic power has been shifting from developed to emerging economies. The competitive environment for financial services in what PwC describes as the SAAAME region (comprising South America, Africa, Asia and the Middle East) has significantly changed as these areas experience accelerated growth and increased intra-regional trade, with Africa in particular being a key part of this growth opportunity.

Yet, for every well-documented description of opportunity across the continent, significant challenges remain. Much of these challenges either relates directly to, or arises indirectly from, poor infrastructural development across vast portions of the continent. At the same time, access to infrastructure services – whether for power, water, freights or communication services – are significantly more expensive as elsewhere. The quantitative cost of inadequate infrastructure development across Africa can be estimated at many billions in lost GDP growth annually.

Financing the African opportunity will need to recognise the importance of alternative funding solutions. This has prompted some commentators to highlight inadequacies and challenges that conventional finance mechanisms have demonstrated in responding to the full realisation of the African opportunity.

THE SEARCH FOR SUSTAINABLE YIELD

While the African funding gap scales up, the next decade’s global economic re-balancing of power will be driven by emerging market countries, particularly those in Asia and the Middle East, many of which are actively promoting the Islamic finance model and seeking out Islamic finance investments.

A clear example of this re-balancing can be seen in the recent phenomenon associated with sovereign wealth funds (SWFs), which have risen as a prominent catalyst within global capitalism. SWFs are state-owned investment vehicles that utilise government wealth from excess reserves or commodity windfalls and invest it for returns in financial markets. A number of SWFs are located in the Middle East and other regions with significant oil, natural gas and other commodity reserves.

Investor response to occasional resistance by African companies to foreign investment has often been to introduce significant debt components to their investment proposition. Consequently, alternative capital and financing options for Africa companies tend to be expensive and short term, with terms offered making bank debt sometimes more attractive (even with high prevailing interest rates).

While emerging market economic growth is still outpacing the developed world, the gap is narrowing. The impact of less favourable fundamentals across some emerging economies has been compounded by concerns that excessive liquidity made available by advanced economies in recent years will be tapered. This changing economic landscape will call for greater focus on alternative funding options, as we explore below.

THE ISLAMIC ECONOMIC MODEL: LINKING THE SHIFTING CENTRE OF GRAVITY TO THE SEARCH FOR SUSTAINABLE YIELD

All of this indicates that a potentially seismic African economic opportunity exists, on the one hand, while a global investor community pursuing a search for sustainable yield in a volatile global economy exists on the other. Given the economic context outlined, new alternative sources of finance will increasingly show heightened demand.

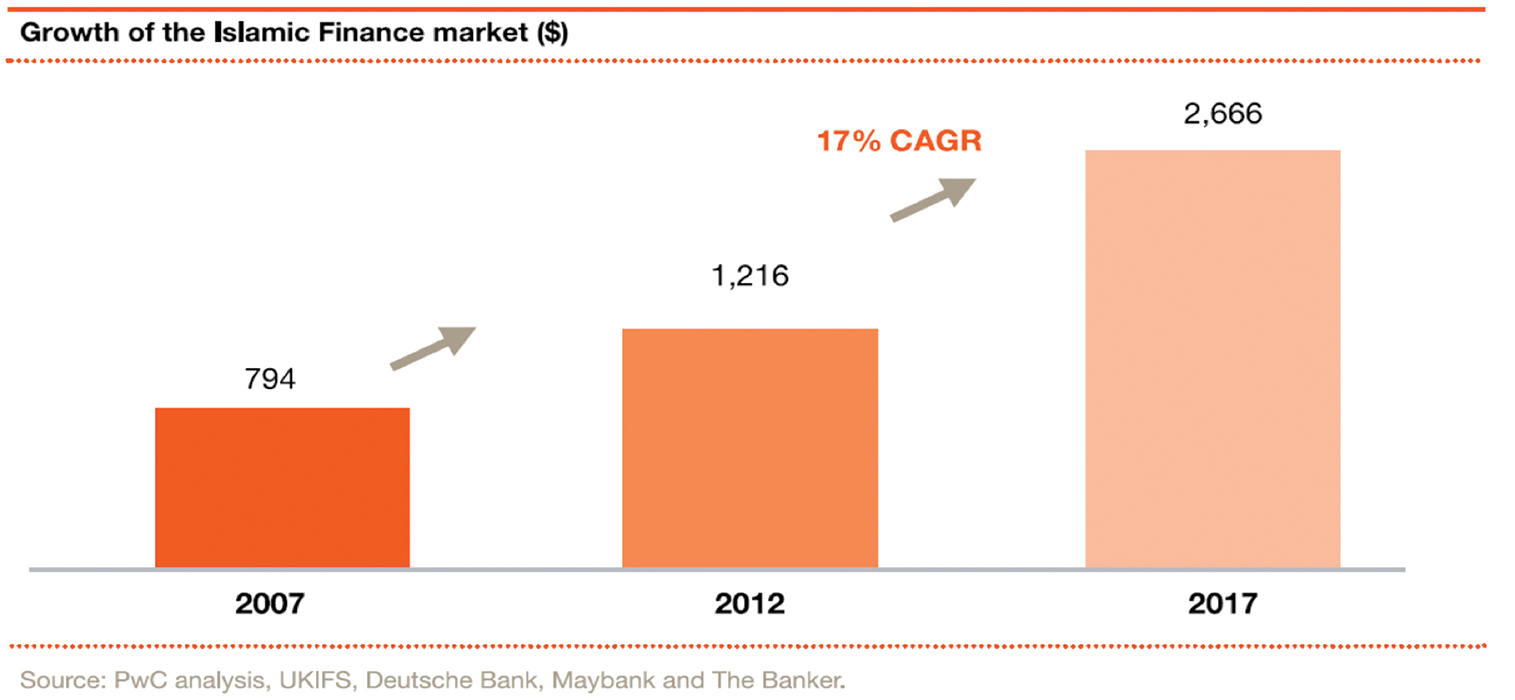

PwC analysis1 reflects that in recent years, Islamic finance has grown rapidly across the world, estimated at 10–15% annually. Our analysis assumes that by 2030 more than 95% of the world’s Muslim population will be located in Asia and Africa – squarely at the centre of the SAAAME opportunity.

Speculation around the future of Islamic finance and its place alongside “conventional” finance is over. Larger global forces are at play that will move the Islamic economic model beyond a faith-based financing alternative. These forces will combine such that Islamic finance will continue to grow, particularly in response to satisfying the rapidly increasing financial services needs of the SAAAME region, including large institutional investors such as SWFs. A key question is how rapidly institutions and countries adapt.

CONTRIBUTORS TO ISLAMIC FINANCE GROWTH

The following are considered the main contributors to the growth of Islamic finance:

- Excess liquidity and strong Middle Eastern economic growth: Middle Eastern investors, as well as SWFs, continue to search for suitable financing alternatives and Sharia-compliant assets.

- Islamic “windows” within banking groups: Several global financial institutions that have maintained a presence in the Middle East and Southeast Asia for several years have developed considerable local experience of these markets and have established business lines known as Islamic “windows”. These “windows” utilise the global experience of these institutions combined with local knowledge and assist with product development that facilitated Islamic finance growth in many countries where these institutions operate.

- Establishment of global standard-setting bodies: The Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI), among other activities, prepares accounting, auditing, governance, ethics and Sharia standards for Islamic financial institutions.2

- Current and prospective regulatory reforms: The implementation of Basel III represents the biggest regulatory change the banking industry has seen in decades. Some observers believe regulatory change will magnify opportunity for innovative capital instruments to be written to support banks’ traditional returns on equity and growth levels.

ISLAMIC FINANCE IN AFRICAN RETAIL AND WHOLESALE MARKETS

Retail markets

To date, South Africa’s major banks have faced challenges in significantly growing their Islamic franchises, which remain a minor part of the banks’ retail operations.

The size of the Muslim population across the African continent, together with differing levels of societal understanding of Islamic finance principles and some of the other challenges outlined below, implies that Islamic finance growth in the retail sector presents a difficult and competitive landscape.

However, given the size of the unbanked population across various countries, the banks that will do well are those that effectively leverage Islamic finance principles in product design, raising public awareness of these principles, while seeking to cast the net capturing the unbanked population wider.

Wholesale markets3

The greatest growth, and perhaps one area with the most significant contribution to the African infrastructure finance challenge, relates to the Sukuk (Islamic bond) market.

In the context of Sharia principles’ general prohibition on interest payments, conventional debt instruments would fall outside the remit of Sharia compliance. Sukuk represents instruments that are structured to generate similar economic effects as conventional debt instruments, in a Sharia-compliant manner through using contractual techniques permissible within Sharia principles.

Structuring Sukuk is, in many ways, similar to securitisation with one common characteristic being that settlements are based on the performance of underlying assets – making Sukuk instruments asset-based rather than asset-backed. Two key differences exist between Sukuk and securitisation. First, for Sukuk there is no de-linkage of the assets from the originator (in other words, there is no “true sale” of the assets by the originator to a special purpose vehicle). Second, investors in Sukuk are exposed to the issuers’ risk rather than the assets’ risk.

To date, no African state has come to market with a sovereign Sukuk offering, although various countries (including Nigeria and South Africa) have expressed interest and announced plans to issue sovereign Sukuk in coming years on the international market. These countries have highlighted Sukuk financing avenue as being a key measure to attract foreign direct investment from the growing economic potential within the SAAAME region.

KEY CHALLENGES TO ISLAMIC FINANCE GROWTH

The following are considered the main challenges to the growth of Islamic finance:

- Balancing a profit motive with risk aversion: The prohibition against interest-related transactions, in effect, handicaps an Islamic financial institution from being able to compete with conventional banks from a profitability perspective. As a case in point, emerging economies generally face the challenge of a lack of sufficiently deep and liquid financial markets compared to advanced counterparts. Banks in emerging markets typically meet statutory liquid asset requirements in the form of government securities, which attract market-determined yields. However, given the Islamic model’s interest prohibition, divergent views may arise as to how an Islamic financial institution should utilise the interest earned on statutory reserves where these are remunerated.

- Domestic legal frameworks across individual jurisdictions on the continent may not be fit-for-purpose to support Islamic finance: Key areas where legal exemptions may be required or domestic legal frameworks may need to be amended include:

- Real estate ownership and taxation laws associated with the transfer or sale of property

- Ownership of and trading in assets and commodities

- Remuneration of mandatory reserves held with central banks

- Deposit insurance

- Arbitrage of Sharia principles: Diversity of opinion exists as to whether particular practices or products are Sharia compliant, which may also depend on the jurisdiction in which they are offered in

- Significant talent shortages of Sharia scholars with appropriate banking experience to approve and monitor products’ Sharia compliance

- Public scepticism given a lack of knowledge and understanding of Sharia principles outside the Islamic community

PROSPECTS

The reshaping of the global economic order is unprecedented in speed and scale. The vast untapped potential of the African continent is positioned to share in the realignment of global business activity and spending power.

As these trends continue, it will have an increasing impact on where growth opportunities arise for companies, where they invest and on how they finance their activities to capitalise on those opportunities.

Given its inherent potential to aid in meeting the deep African infrastructural and other financing challenges, the Islamic finance model has a compelling case to rise as a significant frontier in emerging market banking. With regulatory change impacting business models to a greater degree, and the risk weighting of certain activities influencing the direction in which banks choose to deploy their balance sheets, a trend towards strategically focusing on Islamic financial products represents a sizeable opportunity. Fully capturing and realising this opportunity will require clear and deliberate policy decisions, as well as strategic focus from both financial institutions and governments across the continent.

Notes

1 https://www.pwc.com/m1/en/publications/islamic_finance_capability_statement.pdf.

2 http://www.aaoifi.com/en/about-aaoifi/about-aaoifi.html.

3 Technical references adapted from the UK Financial Services Authority (FSA), Islamic finance in the UK: regulation and challenges (wholesalce markets).

Author: Zuhdi Abrahams CA(SA) is a partner at PwC

A new world for the insurance industry

How companies can best prepare their financial models for IFRS 4 Phase II

After many years of preparation and consultation, the International Financial Reporting Standard (IFRS) for insurance contracts (IFRS 4 Phase II) appears to be finally entering the end game. However, significant topics that are still to be finalised are the treatment of participating contracts and the arrangements for transition of these contracts from the existing reporting requirements (IFRS 4).

During 2014 the International Accounting Standards Board (IASB) spent a substantial amount of time during its re-deliberations on the approach for participating contracts including considering an alternative approach developed by the European industry. The board is considering a number of alternatives for participating contracts and are expected to start making decisions during the February and March 2015 board meetings. The indications are that the IASB is gearing up to publish a finalised IFRS standard late 2015 or early 2016. For many organisations this will represent the beginning of a significant undertaking.

The IASB is expected to allow around three years between the publication and effective date to give both insurers and the markets time to prepare and adjust. An effective date before 2019 is unlikely. This may seem like a relatively relaxed timetable, but in reality it is not. There are a number of other changes that would appear more pressing, including SAM for South African insurers. However, it’s vital to get strategic planning for IFRS 4 Phase II under way as soon as possible. Preparing an opening balance sheet for restated comparatives in 2018 will be the initial focus. Together with IFRS 9 and IFRS 15, this forms a package of changes for insurers to consider. With many of the necessary systems likely to take 18 months to two years to design, install and embed, this is going to be a busy time.

Making the most of the time between now and the effective date, given conflicting priorities, will be an important consideration in ensuring a successful transition to IFRS 4 Phase II. Early evaluation and planning will make it easier to align the data collection, modelling and reporting systems with those already being developed for SAM. The importance of looking at reporting developments together is heightened by the coming changes to financial instrument accounting (IFRS 9) and revenue accounting (IFRS 15) for non-insurance contracts. IFRS 9, in particular, will have close linkage with the new insurance contract standard.

IFRS 4 Phase II is designed to bring greater comparability to what is at present a diverse patchwork of national approaches to liability measurement. The foundations for the new standard are a series of building blocks (building block approach or BBA) for liability measurement. This is the model applied to non-participating contracts.

So how will this work? The standard applies to all contracts that meet the definition of insurance, which depends on whether significant insurance risk is transferred to the insurer, and is largely unchanged from current IFRS 4. The liabilities are measured as the amount required to fulfil the contract over its lifetime, with three components coming together to provide the evaluation:

- The probability weighted estimate of the future cash flows to fulfil the contract discounted for the time value of money

- An adjustment for risk is included to reflect the compensation the insurer requires for bearing uncertainty

- The contractual service margin (CSM), which represents the future unearned profits of the contract to be recognised in profit and loss over the life of the contract. It eliminates any day one gain on the contract by deferring the recognition to future periods. Expected losses on onerous contracts on day one are recognised immediately in profit or lossAs would be expected in an industry with diverse products, there are some exceptions:

- The measurement of contracts with participating features incorporates additional principles to reflect the link to underlying asset returns for these contracts

- For short duration contracts, the business can elect – if certain requirements are met – to apply a simplified model (the premium allocation approach or PAA) to measure the pre-claims liability (liability for remaining coverage akin to the current unearned premium provision). This measures the liability based on the premium received in the period less acquisition costs paid and amounts recognised as insurance contract revenue as a proxy for the BBA model. In the post-claims period, the BBA model is applied for the liability for incurred claimsThe changes in the insurance contract liability measurement for non-participating contracts will flow to the income statement or other comprehensive income as follows:

- Changes in cash flows related to past and current services are recognised in the underwriting result in the income statement, for example, current period mortality experience variance

- Changes in cash flows related to future services are recognised against the CSM, unless the CSM is exhausted. In that case these changes are recognised in the underwriting result

- Entities have an accounting policy choice to recognise changes in discount rates either in the investment result in the income statement or in other comprehensive income

- The release of the risk adjustment relating to the current and past periods is recognised in the underwriting result in the income statement. The update of the risk adjustment for current estimates relating to future coverage is recognised against the CSM

- The release of the CSM according to the services provided is recognised in the underwriting result in the income statement

The proposed “mirroring exception” for participation contracts was challenged by many of the respondents to the 2013 exposure draft due to the perceived complexity (amongst other concerns). As a result, the IASB has spent significant time during its re-deliberations on the approach for participating contracts, including considering an alternative approach developed by the European industry. However, as of the date of this article no conclusions have been reached.

The key areas being discussed for participating contracts include:

- Scope: To which contracts does the separate model apply?

- Splitting of cash flows: Will the requirement to split cash flows in the 2013 exposure draft be amended?

- Determining interest expenses in profit or loss: Two approaches are being explored by the IASB for determining the discount rates used for income statement presentation, namely a “book yield” approach and an “effective yield” approach

- Unlocking and amortisation of the CSM: Will the CSM be unlocked for the movement in the insurer’s share of underlying items?

- Presentation of changes in the value of options and guarantees: Will changes in the value of options and guarantees to be presented in profit or loss or adjusted against the CSM/recognised in OCI?

SO WHAT SHOULD BE THE KEY AREAS OF FOCUS?

- Actuarial systems: New systems and functionality will be needed for the CSM as there is no equivalent concept under SAM or in most current reporting

- Data, interfaces and reporting systems: New data will be required for the liability calculations and reporting disclosures. The level to which calculations are required (unit of account) could have a significant cost implication. The reporting flows and interfaces will require review and possible updating as a result. A fundamentally different style of income statement (notably for life insurers) is also likely to necessitate what could be a significant overhaul of general ledgers, consolidation tools and reporting

- Operating model for Actuarial, Risk and Finance: This standard will require even further collaboration, understanding and consistency across these functions, whether these functions are distinct or integrated

- Strategic implications: As the treatment of participating contracts is still a moving target, this is one area where it is too early to consider changing the business or products

- Management implications: From a management perspective, a significant challenge is identifying the right suite of key performance indicators during this period of change and thereafter

- Other projects and competition for resources: Besides IFRS 4 Phase II, insurers are facing many other challenging projects, such as SAM, TCF and other IFRS developments, to name a few. The insurance industry lacks a pool of skilled resources that can get these projects over the finish line. It is crucial to identify the resources available, increasing the supply of resources available to support the industry and using specialists in the most effective way.While the path to IFRS 4 Phase II has been long, it now appears that the finish line may be in sight. There are a number of key questions that companies will need to address to make sure they are effectively preparing for it:

- Do you understand how this standard could impact your business, both in terms of your results and how much it will cost to implement?

- Are your current actuarial, risk and finance systems equipped to deal with the new IFRS?

- How can you make the most of the synergies with the systems and processes being developed for SAM?

- How will IFRS 4 Phase II affect the volatility and trajectory of earnings?

- Are you aware of the availability of data in your systems for the measurement of insurance contracts on transition and afterwards?

In order to make the best use of the time before the standard will become effective and to effectively manage costs in the long run, it will be important to plan early, identify resources, consider the linkages with other reporting regimes such as SAM, and understand the potential financial impacts. Appropriately considering each of these factors will better place companies to effectively manage the long-term effect of this new accounting standard.

Author: Dewald van den Berg CA(SA) is PwC Director, Financial Services Practice

SMP opportunities in Africa require local expertise

African economic opportunities are attracting small businesses as well as the multinational giants – and they need financial oversight and risk management help that understands local rules

Economic growth in sub-Saharan Africa, on average, currently stands at 4,7% per annum – with several countries achieving 8% or more. In a world where many developed economies are still caught up in a recession, the continent’s success is underpinned by its immense mineral wealth in a high-demand market and increasing levels of political and economic stability. These factors are driving rapid industrialisation, which leads to a fast-growing middle class and the expansion of consumer demand.

Thus it is not surprising that the mining multinationals have been followed by a host of service industry and retail giants such as Shoprite, SAB Miller, Sanlam, MTN, Tiger Bands, Steers, Premier Foods, Nando’s, Joshua Doore and Pioneer Foods into our sub-Saharan neighbours. And wherever large companies set up shop, they need a host of smaller suppliers and service providers. If they cannot find suitable partners in a new country, it creates opportunities for their South African SME partners to expand into those countries too – creating a new class of SME multinationals. However, this expansion brings with it new challenges – particularly when it comes to accounting and oversight.

ADAPTING TO MULTIPLE STANDARDS, TAX AND REGULATORY REGIMES

“The key problem is that there is no such thing as a worldwide accounting standard,” says Bridgitte Kriel, Project Director for Small and Medium Practice at the South African Institute of Chartered Accountants (SAICA). “Every country has its own local regulations and tax regimes, reporting standards and codes of best practice, and while we have the best auditing and financial reporting standards in the world, according to the World Economic Forum, we have to recognise that when small businesses do business across our borders they need to be compliant there as well as back in South Africa. That’s one of the reasons we’re members of the Pan-African Federation of Accountants (PAFA) and so far, we have 37 professional accounting bodies in 34 countries on board, it provides a great platform for local SMPs to establish African associates.”

Vickson Ncube, CEO of PAFA, agrees. “One of the benefits of PAFA is that it makes it easier for small and medium accounting practices (SMPs) in South Africa to expand their operations to the rest of the continent by establishing partnerships with SMPs in other countries. The local knowledge is essential,” he says. “Your partner will know the local laws relating to tax and financial reporting; they will understand the local business culture. Remember, these days an accountant can do more for a small business than just the books – they’re invaluable for advice in long-term business planning, sound financial practice, and risk management. To have someone in that role who understands local conditions makes all the difference.”

In summation, Kriel believes that SMPs are perfectly positioned to support SMEs expanding into sub-Saharan Africa who need tax, accounting and auditing support and an assured level of governance, and reporting standards that comply with IFRS principles. She also believes that South African SMPs are ideally placed to offer this support – as long as they acquire local African partners with first-hand knowledge of the country’s business, legislative and regulation culture, and a similar commitment to IFRS accountability. “The small practices that take full advantage of PAFA and the networking opportunities it provides are going to best at finding those partners. South African SMPs can connect with PAFA at www.pafa.org.za for advice regarding their African affiliates,” she concludes.

Author: Bridgitte Kriel CA(SA) is Project Director of Small Practices at SAICA

{kind=link}