- Overview of 2014‒2015 Local Government Audit Outcomes

- IPSAS Adoption in Africa

- An update on supply chain management reforms

- Creating public value

- Provincial Treasury commits to training future financial leaders

OVERVIEW OF 2014‒2015 LOCAL GOVERNMENT AUDIT OUTCOMES

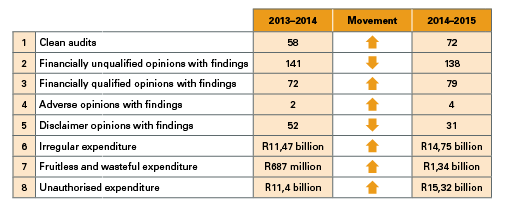

The Auditor-General’s 2014‒2015 report on local government audit outcomes shows a commendable slight increase in clean audit opinions and significant decrease in disclaimer opinions with concerns being raised by the momentous increase in fruitless and wasteful expenditure. By Julius Mojapelo

According to the Auditor-General’s 2014–2015 report on local government audit outcomes, the expenditure budget for the municipal sphere in this period totalled R347 billion.

Municipalities with clean audit opinions represent R134 billion (39%) of this amount, while those with unqualified opinions with findings represent R143 billion (41%). Municipalities with qualified audit opinions made up R49 billion (14%) of the total budget, with those with adverse and disclaimed opinions representing R20 billion (6%).

The outstanding audits constitute R1 billion of the total budget.

In his executive summary, the Auditor-General also stated that an increased accountability and transparency within local government was evident as indicated by the significant improvement made in submission of financial statements for audit by the legislated date and the preparation of annual performance reports.

The financial statement submission rate improved from 78% to 94%, while the number of municipalities that failed to prepare annual performance reports decreased from 14% to 4%.

SUMMARY OF AUDIT RESULTS

The table provides a summary of the audit results as published in the 2014–2015 MFMA consolidated report on the audit outcomes of local government.

Clean audits

A clean audit opinion is given when the financial statements contain no material misstatements and there are no material findings on the quality of the annual performance report or compliance with key legislation.

Financially unqualified opinions with findings

A financially unqualified opinion with findings is given when the financial statements contain no material misstatements, but findings have been raised on either the annual performance report or compliance with key legislation, or both these aspects.

Financially qualified opinions with findings

A financially qualified opinion with findings is given when the financial statements contain material misstatements that are confined to specific amounts, or the misstatements do not represent a substantial portion of the financial statements.

Adverse opinions with findings

An adverse audit opinion with findings is given when the financial statements contain material misstatements that are not confined to specific amounts, or the misstatements represent a substantial portion of the financial statements.

Disclaimer opinions with findings

A disclaimer opinion with findings is given when the auditee provided insufficient evidence in the form of documentation on which we could base an audit opinion. The lack of sufficient evidence is not confined to specific amounts, or represents a substantial portion of the information contained in the financial statements.

Irregular expenditure

Irregular expenditure is expenditure incurred without complying with applicable legislation.

Fruitless and wasteful expenditure

Fruitless and wasteful expenditure is expenditure that was made in vain and could have been avoided had reasonable care been taken.

This includes penalties and interest on the late payment of creditors or statutory obligations as well as payments for services not utilised or goods not received.

Unauthorised expenditure

Unauthorised expenditure is expenditure that was in excess of the amount budgeted or allocated by government to the auditee, or that was not incurred in accordance with the purpose for which it was intended.

AUTHOR l Julius Mojapelo CA(SA) is Project Director: Public Sector at SAICA

International Public Sector Accounting Standards enable governments to account for material liabilities such as debt, pensions and service concessions. By Amon Dhliwayo

From time immemorial, governments have reported in terms of cash basis accounting. Over the past decade governments in Africa, with the aid of the World Bank and International Monetary Fund (IMF), have adopted accrual accounting financial reporting frameworks in the form of International Public Sector Accounting Standards (IPSASs) as opposed to International Financial Reporting Standards (IFRSs).

IPSAS standards are more suitable for public sector entities that operate to deliver services to the public rather than to make profits and generate a return on equity to investors.

IFRSs are developed by the International Accounting Standards Board (IASB) while the International Public Sector Accounting Standards Board (IPSASB), a standard-setting board of the International Federation of Accountants (IFAC), develops the IPSAS standards. These are aligned to IFRS but adapted to a public sector context where appropriate.

IMPORTANCE OF IPSAS ADOPTION

IPSASs comprise a suite of one cash and a number of accrual basis standards and offer governments the flexibility to initially adopt the simpler cash basis standard as a stepping stone to implementing the more onerous accrual basis standards. To add on, IPSASs provide governments with a three-year measurement and recognition relief for certain assets (investment property, property plant and equipment, and biological assets) and liabilities associated with assets that have not been recognised (employee benefits, provisions, and contingent liabilities).

As a result, governments have sufficient time to lay processes and procedures to measure and recognise assets and liabilities so as to comply with the requirements of the IPSASs.

IPSASs enable governments to account for material liabilities such as debt, pensions and service concessions. Currently, most governments do not recognise debt on their balance sheets as they do not know how much they owe and the corresponding cost of debt (interest) thereof. The USA and Greece owe approximately US$19 trillion and US$350 billion respectively and most African countries have amassed debt that exceeds their respective gross domestic products (GDPs).

Governments employ a large proportion of the working population, but the corresponding pension benefits payable to employees on retirement are not recognised on the balance sheet. In November 2015 the Cayman Reporter noted that the Auditor-General of the Cayman Islands had issued an adverse audit opinion citing that the post-retirement pension benefits were understated by approximately US$1,4 billion and urged the government to follow the principles of IPSASs to account for pension liabilities.

Strive Masiyiwa, chairman of the board of the Alliance for a Green Revolution in Africa (AGRA), emphasised to the audience at the 2014 World Food Prize Borlaug Dialogue that present demographic trends indicated that 2,5 out of 10 children born in the world were from Africa. He added that this number was expected to rise to 4 out of 10 children by the year 2050. As a consequence, governments will need to account for social benefit obligations in the form of grants, stipends and welfare benefits. The IPSASB is currently developing a standard that will provide guidance on the recognition and measurement of social benefits.

IPSASs allow governments to report on service concession liabilities incurred from public-private partnerships (PPPs). Governments enter into PPPs with private sector entities to construct, develop and maintain roads for public use and usually incur a liability to compensate the private sector over the period of that agreement.

IPSASB also issued recommended practice guideline (RPG) on service performance which allows governments to report on the efficiency and effectiveness of service delivery in the financial statements. For example, if the objective of the ministry of health at the start of the financial year is to vaccinate 10 000 patients infected with HIV, IPSASs can assist governments to report whether or not the objective was achieved and how efficient that service was provided at the end of the financial year.

CHALLENGES FACED BY COUNTRIES THAT HAVE ADOPTED IPSAS

The adoption of IPSASs is a costly and time-consuming exercise because information systems and processes need to be upgraded, staff trained, and assets verified and valued. The successful implementation of IPSASs is also reliant on the support of politicians and stalls if such form of support is not attained.

The accounts of controlled state-owned enterprises prepared in terms of IFRS also need to be reconciled and adjusted to match the IPSAS financial statements of the controlling public sector entities when preparing the consolidated financial statements of the whole government.

The pace of IPSAS adoption in Africa has been slow as funding received from donors for implementation is usually diverted by governments to other important programmes such as education, health and welfare.

Other countries in Africa have only referenced IPSASs and developed their national standards as opposed to the full adoption of the IPSASs because the standards lacked a Conceptual Framework and there were reservations about the independence, governance and oversight of the IPSASB’s standard setting process. Nevertheless, the IPSASB published a Conceptual Framework in 2014 and established the Public Interest Committee (PIC) and the Consultative Advisory Group (CAG) in 2015 and June 2016 respectively to oversee the governance of the standard setting process.

COUNTRIES ADOPTING IPSAS

African countries

There are contradictory statistics in Africa about which countries have adopted or have complied with IPSASs. Most countries in the African continent have announced their intention to adopt these standards and implementation has occurred in leaps and bounds for reasons mentioned above.

According to a KPMG survey of 21 countries in Africa in 2012, some 62% of local governments adopted accrual accounting while 54% of central governments reported in terms of cash basis of accounting. Some of the countries surveyed were Algeria, Botswana, Gambia, Ghana, Kenya, Mauritania, Morocco, Nigeria, Rwanda, Sierra Leone and South Africa.

In West Africa, Nigeria and Ghana have led the adoption of IPSASs with the former following an aggressive step by step approach over a three-year period, where it first adopted cash basis IPSAS in 2014 and accrual basis IPSAS by 2016. Ghana on the other hand, announced its intention to adopt IPSAS spanning over a five-year period from 2016.

Kenya and Tanzania have led the adoption of IPSAS in East Africa, with Tanzania already producing consolidated financial statements for its central government and national departments.

The progress of IPSAS adoption in North Africa is somewhat unknown.

In Southern Africa, South Africa has referenced IPSASs and developed its own accrual accounting standards known as Generally Recognised Accounting Practices (GRAPs). The central government (National Treasury) has adopted a modified cash basis of accounting framework. However, the National Treasury have developed a roadmap to implement the accrual accounting framework in terms of GRAP at central government.

The government of Botswana is working on a full adoption of the accrual basis IPSASs, while Lesotho, Swaziland. Zambia and Zimbabwe intend to firstly implement cash basis IPSAS as a stepping stone to adopting accrual basis IPSAS.

Most francophone countries in Africa have expressed interest in adopting IPSAS from the year 2017.

Countries outside Africa

There is a lot of IPSAS activity outside Africa. In Australasia, New Zealand has led the implementation of IPSASs and developed their own public sector standards that are based on IPSASs. In Europe, Austria, Russia and Cyprus are at the forefront of implementing IPSASs or referencing it to develop their own public sector accounting standards. The European Union is also developing its own version of IPSASs known as the European Public Sector Accounting Standards (EPSASs).

In the Middle East, Abu Dhabi, Dubai, Jordan and Saudi Arabia lead the adoption of IPSASs while Chile, Colombia and Brazil are on the forefront of adopting IPSASs in Latin America.

Intergovernmental institutions

In addition, major international intergovernmental institutions such as the African Union, the Southern African Development Community (SADC), the World Bank, the European Commission, the Organisation for Economic Cooperation and Development (OECD) and the United Nations have adopted IPSASs.

CONCLUSION

The adoption of IPSASs has not been without challenges. Critics have questioned the suitability of IPSASs as adoption is costly and time-consuming, and the standards seem complex to apply.

Therefore the pace of adoption has somewhat been slow, although many countries are expressing their intention to adopt IPSASs.

On the other hand, the sovereign debt crisis has caused many governments to fail to meet their maturing obligations.Also, poor public financial management practices in the continent have affected the delivery of appropriate services to the citizenry.

As a result of the above the application of IPSASB pronouncements and guidance will enable governments to account to their people on how to tax income received is utilised to deliver services to communities, provide quality education for the youth, pay down its debts, cover social benefits payable to the elderly population, and pay pensions owing to its employees on retirement.

AN UPDATE ON SUPPLY CHAIN MANAGEMENT REFORMS

Supply chain management reforms seek to empower previously disadvantaged groups and work towards creating sustainable business opportunities that will result in the creation of decent jobs and reduce the amount of paper by streamlining the different types of procurement

After the establishment of the Office of the Chief Procurement Officer (OCPO) in the National Treasury, a supply chain management (SCM) review has been published in 2015 highlighting the challenges within the SCM environment across government and proposing the mechanics in the form of reforms to correct these ailing areas.

This was followed by the publication of an update on the progress in March 2016, which included indications of further reforms planned for years ahead.

With regard to the planned work, the OCPO has since June 2015 started reviewing tenders above R10 million across government and its entities to ensure compliance with procurement rules.

The non-payment of suppliers within 30 days remains a challenge across government. The OCPO, in partnership with the Black Business Council in the Built Environment (BBCBE), is establishing a walk-in and call centre to facilitate the resolution of suppliers enquiries related to unpaid invoices.

From information sessions with Parliamentary oversight committees the OCPO was instructed to develop reporting mechanisms on the performance of all government procuring entities to enable oversight committees to diligently do their work. These reporting tools are unpacked below indicating how members of the public and stakeholders in SCM can interpret these to their benefit.

The availability of these reports will enable business (that is, suppliers) to get insight into what is happening in public procurement. This will enable the long-term goal of ensuring that goods, services and works procured are manufactured within the boundaries of South Africa.

WHY WE NEED INFORMED SUPPLIERS FOR SUPPLY CHAIN MANAGEMENT / PUBLIC PROCUREMENT

Through engagements with suppliers, the OCPO established that most suppliers, especially emerging ones, tend to participate only in the quotation systems supplying similar commodities. This leaves the quotation system environment saturated and open to bribery. The SCM environment is made up of different tools that seek to empower previously disadvantaged groups. The interim proposed Preferential Procurement Policy Framework Act (PPPFA) regulations closed for public comment on 15 July 2016. The regulations seek to empower previously disadvantaged groups through public procurement.

WHAT IS THE SCOPE OF GOVERNMENT PROCUREMENT?

Government has close to 780 procuring entities classified into schedules through the Public Finance Management Act (PFMA) and Municipal Finance Management Act (MFMA) to which suppliers can supply commodities and services. The challenge is that most emerging and small suppliers focus on one procuring entity and a similar group of commodities. The table below, drawn from the Central Supplier Database, indicates the commodity and service areas that are saturated.

This list of commodities should be compared to what the DTI has designated to determine if suppliers are taking advantage of the designated sectors.

PROCUREMENT PLANS

The process of supply chain management is indeed a chain that connects many activities and functions within government. First, it ties budget or funds to the plans reflected through the procurement plans. As a start the OCPO publishes the procurement plans for national departments and entities on the eTenders site under Quarterly Scheduled Bid Opportunities for National Departments and Public Entities. The procurement plans give an indication of what government or each department will be buying in a quarter. This allows for suppliers to prepare their resources, do research on how best they can participate in the provision of goods, services and works presented in the procurement plans. They can also follow up with departments to check the delays and possible cancellations of these tenders when they get past the due date for advertising. The provincial treasuries are supposed to do the same for provincial governments.

It is imperative for suppliers to understand that when a tender is reflected on the procurement plan it should be budgeted for. There are huge implications when a tender is recorded in the procurement plan and later withdrawn. This affects service delivery and reflects poor planning on the part of the procuring entity.

AUTOMATION OF SUPPLY CHAIN MANAGEMENT PROCESSES

The automation of SCM processes seeks to reduce red tape for suppliers and users in transacting with government and brings an element of transparency to the entire value chain. The recent development in the automation process introduced the Central Supplier Database, a compliance tool that manages administrative compliance real-time, the eTenders site which publicises all competitive bids from procuring entities, and procurement plans for national departments and public entities. gCommerce is another system intended for internal users who buy from transversal contracts, more like an online shopping system. The commodities from awarded transversal contracts are itemised, codified and loaded on gCommerce.

CENTRAL SUPPLIER DATABASE

The Central Supplier Database (CSD) for government was introduced on 1 September 2015. It became compulsory for use at national level from 1 April 2016 and for local level from 1 July 2016 to coincide with the beginning of the financial year. The CSD automates the verification of tax clearance certificates, company registration information, personal identification and banking information. B-BBEE compliance is not on board due to the changes in the codes. Suppliers are still requested to submit B-BBEE certificates separately. Enhancements are being made to interface with government payroll systems to address the challenge of public servant doing business with government.

The CSD offers more than compliance. It allows suppliers to form partnerships and consortiums in order to bid for larger procurement opportunities. Self-registration on the CSD takes on average 20 minutes (www.csd.gov.za).

THE ETENDER PORTAL

The eTender portal was introduced on 1 April 2015 and contains the following information:

• All bid documents for a particular tender

• The list of tenderers and their respective prices

• Details of the winning bidder, and

• Scores of the rest of the bidders who went through the evaluation and adjudication process

The portal enhances transparency and is expected to reduce corruption and the number of tender disputes over time. Bid documents are made available to bidders free of charge on a single platform that is searchable and accessible 365 days a year. To date, more than 2 800 tenders representing some R40 billion in government business have been advertised on the portal (www.etenders.gov.za).

REVISIONS TO PPPFA REGULATIONS

Review of the current SCM legislative framework is under way. This will culminate in a single public procurement legislation addressing all the legislative and regulatory inefficiency in the system. The Public Procurement Bill will fully establish the OCPO, ensure the SCM system is fair, equitable, transparent, competitive and cost-effective, and provide for an agile system of preference that will support social-economic transformation consistent with section 217 of the Constitution.

In the interim the OCPO, in consultation with business, worked together to revise the PPPFA regulations that were out for public comment closing 15 July 2016. Once the regulations are promulgated, they will introduce the following changes.

30% sub-contracting

In order to further develop emerging suppliers, it will be compulsory to sub-contract a minimum of 30% of the value of the contract for all contracts above R30 million. The tenderer must sub-contract a minimum of 30% of the value of the contract to:

• One or more black female-owned exempted micro enterprises (EMEs), or

• One or more black youth-owned EMEs, or

• One or more black-owned EMEs, or

• One or more qualifying small business enterprises (QSE), or

• One or more small businesses

Pre-qualification criteria

The option to use pre-qualification criteria based on BBBEE levels of contribution has been introduced as a means to further support small and emerging enterprises. Examples of such pre-qualification criteria, although not exhaustive, are:

- The tenderer must have a stipulated minimum B-BBEE status level of contribution.

- The tenderer must sub-contract a minimum of 30% of the value of the contract to one or more black female-owned EMEs, or one or more black youth-owned EMEs, or one or more black-owned EMEs.

Objective criteria

An objective criterion is to be taken into account after price and preference have been evaluated. The organs of state who intend using the objective criteria on evaluation of tenders will be required to indicate in the advertisement of such tenders that the tender will be subject to further evaluation in terms of objective criteria over and above the 80/20 or 90/10 preference point system.

The criteria must be objective and may include, but not limited to, a tenderer sub-contracting a minimum of 30% of the value of the resulting contract to one or more:

- Black female-owned EMEs, and/or

- Black youth-owned EMEs, and/or

- Black-owned EMEs, and/or

- Co-operatives conducting business in the municipal area or province where the goods or services are required, and/or

- Enterprises conducting business in a township or rural area in the municipal area or the province where the goods or services are required, and/or

- Small, medium and micro enterprises (SMMEs)

The introduction of these reforms seeks to empower previously disadvantaged groups and work towards creating sustainable business opportunities that will result in the creation of decent jobs and reduce the amount of paper by streamlining the different types of procurement.

It is worth noting that the SCM environment has multiple stakeholders that work together to the realisation of this objective. The DTI issues designations to drive the development of the manufacturing sector for goods and works within the boundaries of South Africa. More information on these designations can be found at www.dti.gov.za. The Business Development Department should provide programmes to assist and finance emerging business to enter the procurement market.

The Western Cape Provincial Government Treasury head, Zakariya Hoosain, ensures good governance through financial accountability, oversight, and natural optimism. By Monique Verduyn

Good governance paves the way for improved service delivery and accountability.It’s a mantra that Zakariya Hoosain lives by. The head of department of the Western Cape Provincial Treasury is rightly proud of what his team has achieved as a result.

He joined the Provincial Treasury in December 2012 and was appointed to his current position in January 2015. The Western Cape’s Treasury has a track record of receiving clean audits which have been upheld under Hoosain’s leadership.

The province leads the pack in terms of financial governance. It’s an achievement that is viewed as a reflection of the quality of the ongoing support given to departments by the Treasury as well as the commitment to good governance by heads of department and their management teams. This has also resulted in the Western Cape having the country’s best-run municipalities, where residents enjoy better services and economic opportunities than elsewhere in South Africa, according to the Government Performance Index compiled by research and advocacy group Good Governance Africa (GGA).

A KEEN INTEREST IN THE PUBLIC SECTOR

Born and raised in Cape Town, Hoosain qualified as a CA(SA) after passing his professional exam in 2005. His older brother had gone into the profession, exposing Hoosain to it from an early age. When he completed his articles, he joined Transnet as a client manager in group audit, servicing the port operations and rail portfolios. That was where he had his first taste of life in the public sector.

Following that, he joined PwC as a consultant. His entrepreneurial side came into play when he made an ambitious move to Mazars after convincing the firm to let him launch a new risk management, internal auditing, and corporate governance service line.

The majority of his clients at Mazars were public service entities and he spent a large amount of his time advising and consulting on a range of topics, including governance, internal audit, and risk management. He also developed a deep interest in the public sector as a result, becoming the engagement partner for assignments conducted by Mazars on behalf of the Auditor-General of South Africa, which included national and provincial departments and municipal entities.

‘I quickly learned that my qualification as a CA(SA) was an enabler, a door opener, and a confidence builder,’ he recalls.

His attraction to the public sector led to him joining the Treasury after six years at Mazars. In his current position, he is responsible for the money that is allocated to the province from National Treasury, which collects funds via agencies like SARS and divides it up between national departments and provinces. Hoosain’s department, in turn, drives the allocation of that money to the different departments that make up provincial government, sees to it that the systems are in place to spend and account for the money, and that year-end financial reporting is compliant with the accounting standards and the law. His department also oversees the provision of capacity-building and support to the different departments and municipalities in the province.

‘Once we have allocated the funds, we have to ensure it is accounted for,’ he says. ‘We engage with the Auditor-General via the audit process, and we have been successful in making sure that spending is properly reported. We have brought levels of non-compliance and irregular expenditure down consistently over the years and we continue to move in a positive direction. There is virtually no unauthorised expenditure in our provincial departments.’

A COMMITMENT TO MAINTAINING HIGH STANDARDS

Upholding the Western Cape’s reputation for being the top-performing province in South Africa in financial governance is something that Hoosain takes seriously. ‘We maintain a tightly disciplined approach so that we can instil confidence in the taxpayers and investors. They need to know that public money is well accounted for. It has not been an easy achievement, but we now have the results we wanted.’

Ask him what advice he has to offer his peers in other provinces and he’ll tell you that government’s nation- and capability-building agenda is a long-term plan. ‘Change does not happen without effort. You have to make sure you build your teams, both those within the Treasury and those that provide support from the outside. Every accounting officer has a role to play, as does every CFO and every official in the public sector. We have to take collective accountability for the monies entrusted to us. It is crucial to have a strong, capable team to drive the good governance agenda.’

Hoosain says it’s also critical to be realistic about what resources you have on hand and then adjust your programme accordingly. It’s difficult but not impossible, he adds. ‘You need to gear your people to achieve certain milestones, which become the building blocks for the next stage, and that in turn becomes an iterative process. You also have to pace yourself and be clear about what you want to achieve.’

THE PROCESS APPROACH

He advises taking a process approach: when managers use a process approach, it means that they manage and control the processes that make up their organisations, the interactions between these processes, and the inputs and outputs that bind these processes together. Some of the benefits of this approach include the focus on integrating, aligning and linking processes effectively to achieve planned goals and objectives, and facilitating consistent performance which in turn provides assurance to customers about the organisation’s quality and capability. And once you arrive at a certain point, says Hoosain, the approach gains momentum and becomes self-propelling.

The parlous state of the global and national economies has not made his job any easier. ‘We are feeling the pinch,’ he says. ‘The dilemma is how to get more out the money we have when there is less of it. That is currently our single biggest challenge. With an ever-increasing mandate and growing expectations to further improve on our journey of financial maturity, we certainly do not want to go backward. At the bare minimum, we want to at least maintain what we have achieved for now, and continue with progress despite the austere environment, albeit at a relatively slower pace than before. We are currently engaging all our provincial colleagues about navigating through these tough times and it requires a fair amount of leadership from all the other accounting officers.’

What Hoosain finds most fulfilling about his work in the public sector is the role he plays in managing and protecting the province’s finances. ‘We are generally not a citizen-facing department, so when we see that the promotion of accountability has resulted in departments being able to implement new strategies, it’s satisfying. For example, our education department was the first in the education sector countrywide to receive a clean audit last year. From an investor and a citizen point of view, people can be confident that we have sound mechanisms in place to account for public finances.’

He also finds the Treasury’s rollout of its extensive supplier development programme gratifying. ‘We employed the use of simple technology some years ago to innovate on a “register once” principle. This mitigated the need for potential suppliers to register with multiple provincial departments to do business. At the same time, we were able to lever the investment in the technology to manage our compliance mandate.’

It’s one of the few areas in which the department is directly involved with the public and it has made big strides in helping first-time suppliers and entrepreneurs to register on the Western Cape supplier database. ‘Our team is making it easier for people to do business with government,’ he adds. ‘On top of that, the vast majority of our suppliers are paid on time. This is a matter we take seriously as we understand the importance of maintaining cash flow for business.’

The Treasury’s provincial strategic goal – good financial governance – is filtered down into the organisation through a disciplined system. ‘We have a sound performance management framework, and clear roles and responsibilities. We build on the outputs year on year, so we always ask, “what’s next?” There is no opportunity for stagnation.’

Of course, none of this would be possible without a supportive team that have bought into the philosophy of good governance. It’s their collective commitment, he says, that has brought about the success for the benefit of the citizens.

SAICA AND PUBLIC SECTOR SUPPORT

Hoosain has been an active member of SAICA’s Public Sector Committee since 2007. ‘It’s an invaluable platform,’ he says. ‘Firms with an interest in the public sector have the opportunity to discuss issues with key stakeholders, including the Auditor-General, private sector audit firms, the education sector and government, with SAICA facilitating. It’s an active forum that meets every quarter and has clear targets and deliverables. We discuss challenges facing the profession, and often we can pre-empt or resolve them in that forum.’

Hoosain is actively promoting the entry of CAs(SA) to the public sector because of the need for ethical, problem-solving, strategic thinkers in government. ‘The CA(SA) training programme affords trainees the benefit of different perspectives and unique ways to solve problems, and it gives them a set of competencies that are needed to address the growing reporting demands in the public sector, which are arising as the sector prepares for its long-term migration to accrual accounting.’

He says his own training as an auditor has helped to drive Treasury’s financial management maturity agenda and the strengthening of controls in the organisation. Blending the CA(SA) skills set with those of economists, supply chain professionals, management accountants, and financial reporting specialists have given the Treasury an excellent balance of complementary skills.

When he joined the Treasury, one of his early projects was to launch a CA(SA) training academy in order to encourage more young people to enter the public sector and bolster the skills needed in the long run for the accounting transition. ‘We got the programme formally approved in 2015 and the first trainees joined us in March this year. That means that in addition to competing with the private sector, we are also growing and developing our own future pipeline. It’s a pet project of mine, and I’m excited that in three to four years’ time, we will have our first specialist public sector CAs(SA).’

THE IMPORTANCE OF FAMILY

Describing himself as relaxed and easy going, Hoosain says his wife and three children are key to keeping him grounded in such a highly pressurised work environment. ‘My family reminds me that what I do at work is not only for them but for the greater good of all citizens. People generally join the public service because they want to make a difference and my home life is a constant reminder of that. Finding balance in this demanding environment is not easy, but it must be done. As important as the work is, equally significant is the role of my family. I wouldn’t be where I am without their support. Family, at a basic level, is what communities are made up of.’

In addition to the support he receives from his family, Hoosain also has a positive attitude to his work. That helps in a lot in a tough environment that demands hard work and long hours. After all, strict budget timelines wait for no-one. It’s also the kind of setting that demands solutions to daily challenges. ‘Again, that is why it’s so important to be solutions-focused,’ he says. ‘I never feel that any task is too big. No matter what arises, I am guided by my skills set and my optimism.’

PROVINCIAL TREASURY COMMITS TO TRAINING FUTURE FINANCIAL LEADERS

The Western Cape Government Treasury has launched the Chartered Accountants Academy to grow the public sector pool of CAs(SA). Monique Verduyn reports

Sound financial management is the cornerstone of a well-run provincial government. However, entrenching a culture of financial leadership, accountability and ownership is dependent on having the right resources available. The Western Cape Government Provincial Treasury has taken its commitment to good governance a major step forward with the launch of the Chartered Accountants Academy (CAA), which will enable the province to grow its own pool of financial leaders.

Under the leadership of the Head of Department of the Western Cape Provincial Treasury, Zakariya Hoosain; the Deputy Director-General of Governance and Asset Management, Aziz Hardien; and the Manager of the CAA, Adila Aboo, the CAA opened its doors to seven CA(SA) trainees in March 2016. The training conforms to the South African Institute of Chartered Accountants (SAICA) requirements, while simultaneously affording the trainees the opportunity to specialise in the public sector. A requirement for entry into the programme is a Certificate in the Theory of Accountancy (CTA) or equivalent from a SAICA-accredited university, or registration for the CTA.

‘The CAA was established to address the shortage of financial skills in the public sector,’ says Aboo. ‘Instead of hiring CAs(SA) from the private sector, we made the decision to grow and develop our own set of trainees who are at a life stage when they are most open to new ideas and ways of doing things that are specifically in line with our own needs and functions. Because we have aligned ourselves with Government’s National Development Plan (NDP) and its commitment to building a capable state, the training focuses on developing public sector financial specialists.’

The CAA team was responsible for gaining accreditation for the CAA, registering it as a training office, and aligning the training programme with SAICA requirements. In addition to building capacity at the Provincial Treasury, the CAA programme is linked to the Western Cape Government’s fifth strategic goal, which is embedding good governance, and integrated service delivery though partnerships and special development.

The seven trainees, Taryn Jacobs, Sinazo Mtuzula, Tracy-Leigh Lyner, Ayesha Phillips, Kabelo Mafiri, Lulamile Somngcuka and Mogamat Ameer Faker, receive on-the-job technical training through placement at different provincial government departments and institutions on a rotational basis.

‘This first cohort was recruited through cooperation with the province’s universities,’ says Aboo. ‘We were fortunate that the trainees, many of whom had coincidentally already completed the University of Cape Town Postgraduate Diploma in Public Sector Accounting, had not yet signed with other firms. It was obviously “meant to be” as they are the best candidates we could have hoped for and have thus far demonstrated a perfect fit with our organisation.’

Aboo says the aim is to retain the trainees within various spheres of government, thereby encouraging them to remain in the public sector once they have completed the programme. ‘On top of the training, we also place a strong emphasis on developing leadership and management skills, such as creating a thinking environment, managing conflict and building relationships The trainees are part of building the CAA brand, as they will be our future ambassadors.’

Looking ahead, the Western Cape Provincial Treasury wants to gain accreditation for the CAA to accommodate up to 30 trainees. ‘Within just four months, the trainees have added value through their roles at different departments. Now they are in demand, which is an indication that more young people need to be brought into the programme.’

Chartered accountancy students who are interested in applying their financial skills to help make a difference to the country will find that the Western Cape Provincial Government is an excellent training ground, Aboo says. Officials have embraced the programme and are willing to teach trainees in a supportive environment where the focus is on learning and development.

‘The public sector is unknown territory for young people who have been far more exposed to the Big Four firms, but they need to be aware that there is huge variety and opportunity for learning in the public sector,’ she adds. Anyone with strong values and a desire to help grow and change South Africa for the better will be richly rewarded in this space.’

WHAT THE TRAINEE CAS(SA) HAVE TO SAY

Taryn Jacobs

‘The CAA programme is a great opportunity for prospective CAs(SA) who wish to specialise in the public sector. We as young individuals are able to add value and make a difference as we are encouraged to give ideas and voice our opinions, providing a platform for both personal and professional growth.’

Sinazo Mtuzula

‘The CAA programme in the public sector has given me a platform to develop my career objectives which are not only to be a CA(SA) but also to be able to make a difference in people’s lives.’

Tracy-Leigh Lyner

‘The CAA programme has given me the opportunity to not only gain invaluable experience and knowledge in the public sector, but also to know that at the end of the programme, I will be equipped with the expertise to contribute towards the economic growth and development of this country.’

Ayesha Phillips

‘My knowledge on the public sector has been greatly expanded since I’ve started the CAA programme. I believe that the exposure that I have received, and will continue to receive in this programme, will ensure that I am well equipped to be a successful CA(SA).’

Kabelo Mafiri

’Integrity, value adding and capacity-building – these are among the pillars on which this programme is built. Being a part of it and everything it stands for, has been nothing less than extraordinary.’

Lulamile Somngcuka

‘Joining the CAA means that the future is bright for me and I will utilise the opportunity to the best of my ability. My main goal is to add value to the public sector while I gain as much experience as possible.’